Table of Contents

Law firm accounting... yawn!

Just hearing the words makes us want to fake a Wi-Fi outage and go get coffee.

But here’s the deal: If you’re running a law firm, your legal accounting and bookkeeping can't be ignored.

So, a few questions come to mind...

- How do you keep your books clean without losing your mind?

- How do you handle client trust accounts without committing a career-ending ethics violation?

- Is there a way to track your revenue without staring at boring spreadsheets?

Good news: You don’t need a miracle!

We’re breaking down 12 law firm accounting best practices — all in plain English, and with just enough humor to keep you awake.

Top 12 Law Firm Accounting Best Practices

Even with a full calendar, you can still make time to tackle law firm bookkeeping and law firm financial management. We're not kidding. The basics aren’t as scary as they sound — and with these 12 tips, you’ll catch on fast.

1. Yes, You Need to Hire a CPA

Look, you’re great at law. But legal business accounting? That’s a whole different ball game- with rules, risks, and ethics issues you don’t want to accidentally break.

We're going to hold your hand when we say this... hire a pro.

A qualified accountant for law firms knows three things: jurisdiction-specific rules, trust accounting requirements, and how to keep your finances audit-proof.

Here’s how to hire smart:

- Write a clear job description outlining required skills (financial analysis, trust accounting knowledge, legal terminology, etc.).

- Screen for experience with law firm accounting software and local compliance rules.

- Ask open-ended questions in interviews about their experience managing law firm finances.

- Verify certifications and references, including checking with your state licensing board.

- Provide onboarding and training to ensure they’re ready for your firm’s needs.

- Offer competitive pay and benefits to attract top talent in law firm accounting services.

Questions to Ask When Interviewing Bookkeepers and Legal Accountants

- Are you familiar with trust accounting and jurisdictional rules?

- What legal accounting software do you use?

- Have you worked with firms similar to ours?

- Can you help with financial reporting and compliance?

- What’s your experience with tax planning for law firms?

Bonus Tip: Hire a CPA for Next-Level Support

If you want more strategic help, a CPA who specializes in law firm financial management can assist with:

- Financial strategy

- Tax planning

- Tax compliance

- Lease negotiations

- Treasury management

- Financial reporting

Hiring now can save you from big headaches later on.

2. Figure Out What Types of Bank Accounts You Need

All law firms must have bank accounts to handle the flow of revenue, payments, and other funds. Generally speaking, most lawyers use three types of law firm financial accounts:

- IOLTA accounts

- Checking accounts

- Savings accounts

Many law firms have all three accounts or more, depending on their needs. Proper law firm accounting and financial management can help you decide which ones are right for you and which banking institution is suitable for your firm.

When deciding which accounts you should open for your law firm, you'll want to get answers to a few key questions. You should pose these questions to the institution handling your business bank accounts:

- What are the fees involved, and how can they be avoided?

- Are business savings accounts available?

- Are business credit cards and lines of credit available?

- Are IOLTA and other types of trust accounts available?

- Can I designate separate users to handle certain banking matters?

- What type of security and fraud protection do you offer?

Comparing different banks' answers to these questions will help you decide which institution and account are right for you. Shop around and ask lots of questions.

3. Open Three Key Accounts

Once you pick a bank (preferably one that understands law firm accounting services), you’ll want to set up three key accounts as we talked about before:

- Business Checking Account: This is where your revenue lands and where you pay your day-to-day expenses — rent, payroll, office snacks, the works.

- Business Savings Account: Think of this as your financial safety net. Use it to stash cash for taxes, emergencies, or future growth moves. Bonus: You have a better chance of getting a business loan if you have a healthy savings balance.

- IOLTA (Interest on Lawyers Trust Account): This is non-negotiable if you handle client funds. It keeps client money separate from your operating funds (as required by law) and holds it in trust until it’s rightfully earned or disbursed.

Want to get fancy? You could also open a money market account for better interest on your savings — but just know it may come with higher balance requirements and withdrawal limits.

Pro tip: Don't be the awkward Andy who shows up to open your accounts empty-handed. Before heading to the bank, double-check what documents you’ll need! Usually, that means proof of business registration, your firm’s EIN, and your business name details.

4. Get Crystal Clear on the Rules of Trust Accounts

Let’s talk about the elephant in the room: Client trust accounting.

This is where a LOT of law firms accidentally screw up.

Why? Because the rules are strict, the margins for error are tiny, and the consequences (hello, disbarment) are real.

That’s why having a solid grasp of legal business accounting is essential. Here are the non-negotiables for handling your trust account:

- Keep it completely separate: Open a dedicated IOLTA (Interest on Lawyers Trust Account). Mixing client money with your operating funds is a fast track to career regret.

- Follow your state’s rules: Trust accounting rules vary by state. Always check with your State Bar Association and work with an accountant for law firm operations who knows the ropes.

- Never “borrow” from the trust account: Even if you “plan to pay it back,” don’t touch unearned client funds for business expenses. Not now. Not ever.

- Transfer earned fees promptly: Once you’ve earned the money (per your client agreement), move it to your business checking account. Letting it sit in trust longer than necessary? Also, a violation.

- Don’t record trust deposits as income: Client funds sitting in trust = liability, not revenue. Misclassify this, and your books (and ethics record) will both be a mess.

- Track every penny: Maintain detailed, client-specific ledgers with clear transaction history and reference numbers.

- When in doubt? Call in a pro: If you’re unsure, reach out to a legal accountant or a practice management advisor. Many offer confidential advice to help you fix issues before they escalate.

When it comes to trust accounts, it’s better to ask a hundred questions than to end up on the wrong side of an audit.

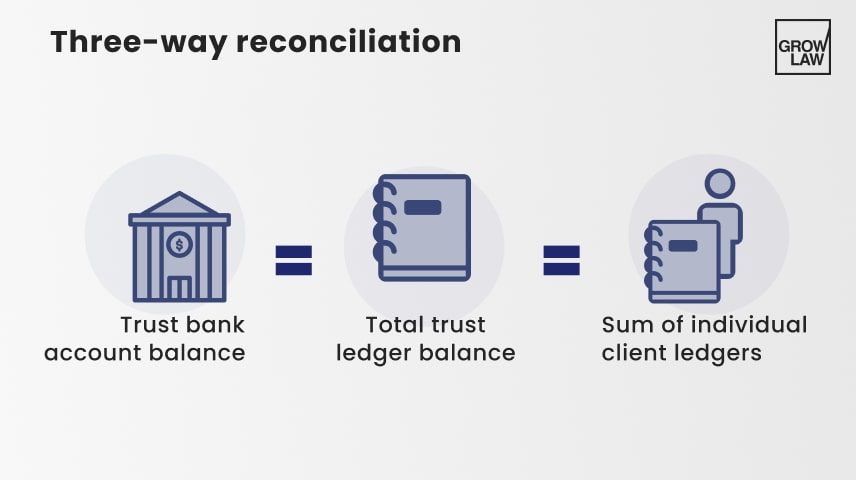

5. Get Ready for Three-Way Reconciliation

If you manage a trust account, three-way reconciliation is a requirement from most State Bars. And yes, they can ask to see your records at any time.

Here’s how it works: Have you ever double-checked that your business checking balance matches your books? Congrats — you’ve done a two-way reconciliation.

A three-way takes it up a notch. You’re matching:

- Your trust bank account balance

- Your total trust ledger balance (the combined total for all clients)

- The sum of individual client ledgers (what each client has in trust)

If even one number’s off? That’s a red flag, and you’ll need to comb through your transactions line by line to find the error.

Most states require you to do this every 30 to 90 days (check your State Bar’s exact rules).

You can go old school and do it manually… or save your sanity and invest in law firm accounting software built for legal business accounting tasks like this.

Reconcile early, reconcile often… and avoid turning your next audit into a full-blown panic attack.

6. Specify Your Accounting Methods

Decision time! When it comes to law firm bookkeeping, you’ve got two main accounting methods: cash accounting and accrual accounting.

Let's break them down!

Cash Accounting: Simple, Sweet, and (Mostly) Stress-Free

With cash accounting, you record income when you actually receive the money, and you log expenses when you actually pay them.

Example:

Client sends a payment → You deposit it → Now it counts as revenue.

You pay for office supplies → Money leaves your account → Now it counts as an expense.

Pros for Law Firms:

- Simplicity: It’s easy to track. Great for solos and small firms without complex billing cycles.

- Tax Timing: You’re only taxed on money that’s actually in your bank account. No need to pay taxes on receivables you’re still chasing down.

- Better cash flow visibility: You’ll always know exactly how much spendable money you have.

Cons:

- Limited financial forecasting: Cash accounting doesn’t show income you’ve earned but haven’t collected yet (aka, your accounts receivable).

- May not scale well: As your firm grows, this method might leave gaps in your financial reporting.

Accrual Accounting: More Complex… But More Accurate for Growing Firms

With accrual accounting, revenue and expenses are recorded when they’re earned or incurred, not when money changes hands.

Example:

Send an invoice today? It counts as income today, even if the client pays three months later.

Receive a bill? It goes on the books now, even if you don’t pay it until next month.

Pros for Law Firms:

- More accurate financial reporting: You’ll get a clearer picture of your firm’s financial health over time.

- Better for long-term planning: Great for firms with lots of ongoing cases, retainers, or deferred billing.

- Required for larger firms: Once you hit a certain size or revenue threshold, the IRS may require you to use accrual accounting.

Cons:

- More complicated bookkeeping: You’ll need a solid system (or a pro handling your law firm accounting services) to stay on top of it.

- Tax liability can hit early: You could owe taxes on income you haven’t even collected yet.

Bottom line:

For solo and small firms focused on short-term cash flow, cash accounting usually makes sense.

For growing or mid-size firms with complex billing, accrual accounting gives you the long-game financial visibility you’ll need.

If you’re unsure, talk to an accountant for law firm finances who understands legal business accounting. Don't let the IRS make the decision for you.

7. Master the Art of Recordkeeping

Trust us — digging through old emails and shoe boxes at audit time is NOT fun.

Law firm bookkeeping lives and dies by your recordkeeping. If the IRS or your State Bar ever comes knocking, “Oops, I lost that receipt” won’t win you any sympathy.

Good recordkeeping isn’t just about compliance — it’s about protecting your firm, spotting financial trends, and making tax season way less painful.

Here’s what you’ll want to keep organized:

- Receipts

- Bank and credit card statements

- Bills

- Canceled checks

- Invoices

- Proof of payments

- Financial statements from your bookkeeper or accounting platform

- Past tax returns

- W2 and 1099 forms

- Accounts receivable reports showing billed receivables

- Case time records (per client)

- Time summary reports by attorney and by client (tools like Clio can help)

- A running register of cases in progress (sorted by client name)

Pro tip: Cloud-based legal business accounting tools like Clio make this way easier to track.

8. Develop a Law Firm Bookkeeping System

Alright — you’ve got your business accounts set up and you’re (hopefully) following the trust accounting rules.

Now let’s talk about the daily grind that keeps it all running: law firm bookkeeping.

A solid bookkeeping for attorneys system keeps your financial house in order and gives you the data you need to make smart business decisions.

So, what does legal bookkeeping actually involve? Here’s the short list of must-do tasks:

- Data entry for all financial transactions

- Posting debits and credits

- Monthly bank reconciliations

- Generating financial reports (so you actually know if you’re making money)

- Creating and tracking customer invoices

- Recording incoming payments

- Processing vendor invoices and tracking firm expenses

- Managing general ledgers and historical accounts

- Running payroll (because your team likes to get paid—go figure)

Hire in-house help, use an outside provider, or invest in law firm bookkeeping services. The key is consistency.

Because when bookkeeping for attorneys gets sloppy, trust us… the IRS and your State Bar notice.

You’ve Got the Bookkeeping — Now Let’s Add the Bookings

Law firm bookkeeping is great. But marketing is what fills the books.

Get More Leads Online

9. Check Your Tax Filings

You’ve got your law firm bookkeeping system humming along (high five for that). Now comes the next survival task: filing your taxes correctly and on time.

This isn’t just about your annual return. Law firms typically deal with:

- Quarterly estimated tax payments

- Payroll taxes (if you have employees)

- State and local tax obligations

- Any trust account-related reporting requirements

Missing a deadline — or filing inaccurate numbers — can lead to penalties, audits, and a lot of stress you really don’t need.

If tax codes aren’t your thing (and let’s be honest… they’re no one’s thing), hire an accountant who understands legal bookkeeping and law firm financial management.

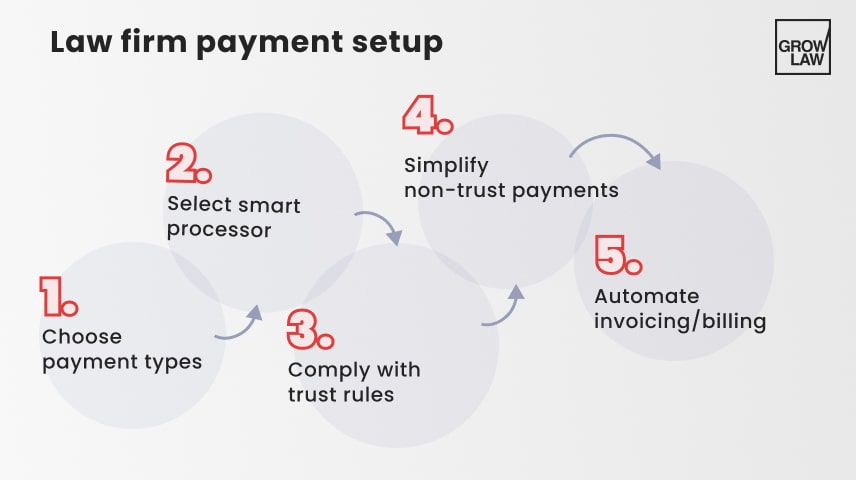

10. Set Up Payment Processing for Your Law Firm

You’ve done the work… now make it easy for clients to pay you!

Let's talk about setting up payment processing for your law firm. This is a must for both your cash flow and compliance.

Step 1: Choose Your Payment Methods

Most State Bars allow debit cards, credit cards, and electronic payments, but always double-check your state’s rules before moving forward.

Step 2: Pick the Right Payment Processor

Not all processors play nice with legal bookkeeping rules. Review fee structures carefully so you know how much each transaction will cost you.

Step 3: Stay Trust Account Compliant

If you handle trust funds, generic platforms like PayPal or Stripe could get you in trouble. Stick with law-firm-specific processors like LawPay or LawCharge, which automatically route processing fees to your operating account, not your trust account.

Step 4: No Trust Account? Keep It Simple

If you don’t deal with trust accounts, Square is a straightforward, affordable option for basic card payments.

Step 5: Automate Your Invoicing

Save time (and headaches) by using legal billing tools like FreshBooks for recurring invoices, online payments, and expense tracking.

Bottom line: The easier you make it for clients to pay, the faster your cash flow improves... and the fewer awkward “Where’s my check?” conversations you’ll have.

11. Automate Your Budgeting

Okay, we're making progress. Now let's tackle your budgeting. Are you currently using a “hope for the best" strategy? If so, it's time for an upgrade.

Start by creating a simple, realistic budget that tracks revenue, expenses, and profit goals. Then automate it. Set up reminders, spending alerts, and monthly check-ins using legal bookkeeping tools or law firm accounting software.

Platforms like QuickBooks or Clio Manage make it easy to keep your budget on track, without drowning in spreadsheets.

12. Using Soft to Make Legal Accounting Easier

Law firm bookkeeping solutions blitz those 3 AM work sessions.

The right software can save you time, reduce human error, and help you stay compliant, without making you hate your life.

Here are five top tools law firms swear by:

- Clio Manage: Combines case management with built-in time tracking and billing — perfect for syncing legal work with your accounting process.

- CARET Legal: A robust practice management platform with tools for accounting, timekeeping, billing, and document management all in one place.

- CosmoLex: Designed for law firms, it handles trust accounting, billing, and matter management — no extra plugins needed.

- QuickBooks (with LeanLaw or other legal integrations): QuickBooks offers strong general accounting features, and when paired with LeanLaw or similar add-ons, it becomes law-firm-friendly for time tracking and reporting.

- LawPay: A payment processing platform built for lawyers, helping you accept client payments while staying trust account compliant.

Want a full breakdown? Check out our Best Law Firm Accounting Software guide for more details.

When it comes to law firm bookkeeping solutions, having the right tools is half the battle won!

Key Terms in Legal Accounting

We get it. Law firm accounting sounds fancy, but it’s really just about keeping track of your money and staying out of trouble. No accounting degree needed, promise!

Let’s break down a few key terms (like trust accounting and three-way reconciliation) so you can stay compliant and profitable.

— Trust Accounting

What happens to client money that isn’t yours yet?

That’s where trust accounting comes in. Think settlement funds, retainers, etc. — money you’re holding but haven’t earned. Your job is to keep it safe, separate, and fully documented.

Key trust accounting rules for law firms:

- Never use trust funds for business expenses.

- Deposit client money into a dedicated trust account (usually an IOLTA).

- Keep firm and client funds 100% separate.

- You can’t keep interest earned on trust accounts.

- Transfer earned fees promptly—don’t let them sit.

- Don’t touch disputed funds until resolved.

- Give clients full accounting on request.

- Reconcile your trust account regularly (see step 5).

— IOLTA

IOLTA stands for Interest on Lawyers Trust Accounts — a pooled account for client funds like retainers and settlements.

The key rule? Your firm doesn’t keep the interest. It goes to state-run programs like legal aid. Here are some IOLTA basics:

- No borrowing or using client funds for firm expenses

- Only withdraw money after it’s earned

- Track each client’s balance separately, even within the pooled account

State rules vary, but one universal truth: Mishandling an IOLTA means serious trouble.

— Double-Entry Accounting

Double-entry accounting is the checks-and-balances system for your firm’s finances. For every transaction, there’s a matching and opposite entry — one debit and one credit — that keeps your books balanced.

Here’s the simple math behind it:

Assets = Liabilities + Equity

That means anytime money moves — whether it’s income or expense — it impacts at least two accounts. Pay office rent? That’s a credit to cash and a debit to expenses. Get paid by a client? Debit cash, credit revenue.

Why does this matter for law firm bookkeeping?

Because it helps catch errors fast. If your debits and credits don’t match, something’s wrong — and you’ll know before it snowballs into a bigger problem.

— Chart of Accounts

A Chart of Accounts (COA) is your law firm’s financial roadmap. It’s a categorized list of every account you use to track money coming in and going out. A well-organized COA keeps your law firm's bookkeeping clear, compliant, and easy to analyze.

Here’s a sample law firm Chart of Accounts setup:

- Assets: Operating Account, IOLTA Trust Account, Client Cost Advance Account

- Liabilities: Client Trust Liabilities, Credit Cards, Loans Payable

- Equity: Owner’s Equity, Retained Earnings

- Income: Retainer Fees, Contingency Fees, Hourly Billing Revenue

- Expenses: Payroll, Office Supplies, Marketing, Rent, Professional Services (like legal research tools)

Pro tip: Customize your COA based on your firm’s billing structure and state bar reporting requirements.

Common Legal Accounting Mistakes to Avoid

Even smart lawyers make sloppy law firm bookkeeping mistakes. Here are five big ones to dodge:

Commingling client and firm funds

Mixing your money with client trust funds is a fast track to ethics violations. Keep every dollar in the right account —always.

Failing to reconcile trust accounts

Trust accounts require regular (often monthly) reconciliation. Skipping this step can hide errors — or worse, violations that’ll trigger bar complaints.

Ignoring accrual-based expenses

Expenses incurred but not yet paid still count. Forgetting them makes your financial reports inaccurate and can wreck your budget planning.

Using personal accounts for business

Running firm expenses through your personal checking account muddles your books, complicates taxes, and raises red flags during audits.

Missing deadlines for tax filings

Late or missing tax payments lead to penalties, interest, and unnecessary IRS attention. Stay ahead with automated reminders or professional help.

Transform Your Law Firm's Financial Systems with Molly McGrath, Founder and CEO at Hiring and Empowering Solutions

In the episode, Sasha and Molly delve into revolutionary methods for improving law firm finances. Molly emphasizes the importance of investing in team development, adopting innovative financial models like Profit First, prioritizing relaxation and system refinement, and restructuring the hierarchy to empower support staff. These strategies collectively contribute to boosting firm income and overall financial success.

Molly McGrath

Hiring and Empowering SolutionsHiring and Empowering Solutions

Molly McGrath is the Founder and CEO of Hiring & Empowering Solutions. She specializes in helping businesses attract, hire, and develop top talent. With a focus on leadership, team engagement, and retention, Molly empowers organizations to build high-performing, people-first workplaces.

Bookkeeping Keeps You Compliant… But It Won’t Fill Your Calendar

Getting your law firm's bookkeeping in order is a huge win.

But let’s be real, clean books don’t pay the bills. Clients do.

If you want to turn that financial stability into real growth, you need a steady flow of qualified leads walking through your (literal or virtual) door.

That’s where we come in.

Grow Law is a law firm SEO agency, having helped over 100 attorneys boost their caseloads with ROI-first SEO, PPC, and web design services — driving up to:

- 1,018% more qualified leads

- 400% to 800% ROI on marketing spend

- 100% transparency and full ownership of your campaigns

Want to see how it could work for you?

Heads up: Your competitors won’t love this… but your revenue will.

FAQs

Compare Your Practice Instantly

Stay Ahead of the Competition!

Compare your law firm's performance to Local competitors with our instant assessment tool

Get a clear picture of your firm's performance

Boost your online presence

Compare My Firm

Compare Your Practice Instantly

Stay Ahead of the Competition!

Compare your law firm's performance to Local competitors with our instant assessment tool

Get a clear picture of your firm's performance

Boost your online presence

Compare My Firm

Check Your AI Visibility Instantly

Find Out What AI Is Telling Your Potential Clients

Run our free AI Grader to:

See how often top AI tools mention your law firm

Spot which competitors show up first

Get the next steps to capture more cases

Run My Free AI Report